We’ve just finished the September Air Travel Organiser’s Licence (ATOL) renewal, traditionally the busier of the two annual rounds, when most of the larger tour operators apply to the Civil Aviation Authority (CAA) to renew.

Applicants must state how many passengers they expect to carry over the following 12 months. The authorisations are a great indication of travel companies’ intent and a trend analysis treasure trove!

Below are three takeaways from our deep dive into the September 2022 authorisation data.

1 – Total ATOL authorisations are back to 2019 levels

Total ATOL authorisations are now slightly above where they were at the end of September 2019.

At an overall level, this would suggest travel companies are expecting next year’s demand will be back to pre-pandemic levels.

In reality, there is a wide range of expectations.

For example, among the top 20 ATOL holders, only six have higher limits than in 2019 (with increases ranging from +1% to +35%).

Conversely, ten of the top 20 companies are more pessimistic than they were in 2019 (with authorisation limits ranging from -4% to -42% below 2019).

Outside of the top 20, the total ATOL authorisations are just 74% of 2019 levels.

There are several possible reasons for this.

Rampant inflation, increasing interest rates and flip-flopping government policies make it incredibly difficult to predict how booking patterns will pan out. For travel companies that pay for bonding, there is little benefit in forecasting overly confident expectations now and incurring costs unnecessarily when they can always apply to increase their limits later in the year.

Another possible reason for the reduced licence limits is Brexit. After 31 December 2020, sales to customers in the EEA could no longer be protected by the ATOL scheme. These customers had to be protected under local equivalent schemes and, therefore would not be included in ATOL projections from that date onwards.

2 – Travel companies are moving out of the flight-inclusive package market.

There has been an exodus of operators from the flight-inclusive holiday market. There are now almost 250 fewer trading ATOL holders** than before the pandemic, representing 14% of the total population.

The pandemic had a severe impact, highlighting the costly obligations that face companies selling ATOL packages. Many came under severe cash flow pressure, stuck between the legal requirement to refund consumers within 14 days of cancellation, whilst unable to recover funds from suppliers. On top of this, the CAA began a consultation on ATOL reform which included some fairly onerous proposals to enforce escrow or trust accounts.

As a result, a number of ATOL holders collapsed. Whilst many others made pre-emptive decisions to pivot away from selling ATOL packages towards less risky business models, like acting as agent, selling single travel components, or non-flight packages.

Whilst the market is much smaller, it hasn’t all been one-way traffic. We’ve seen quite a few new entrants since 2019, notably easyJet Holidays, Booking.com, and a relaunched Thomas Cook, together licensed for 2.6 million passengers.

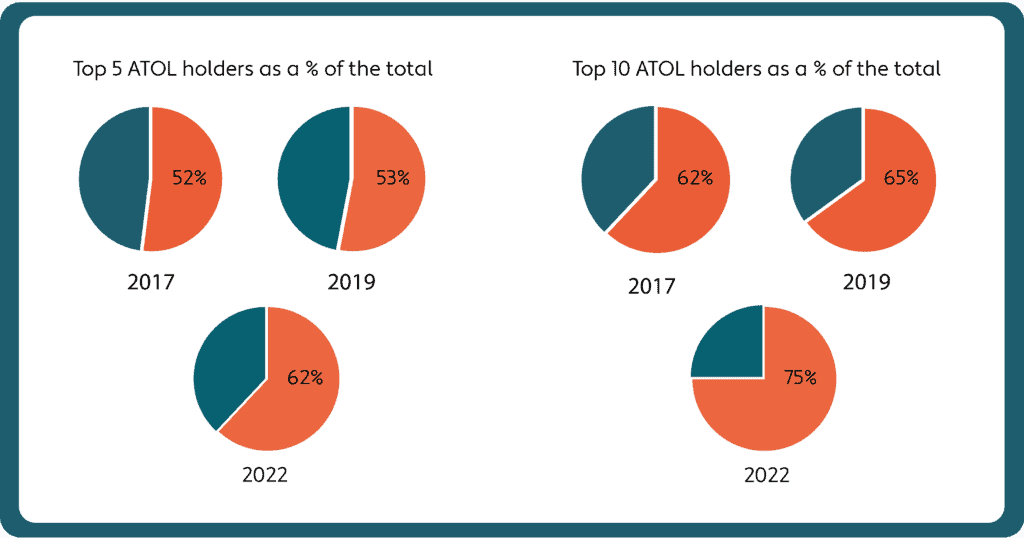

3 – The ATOL market is consolidating

The ATOL package market continues to consolidate. The largest five ATOL holding groups in 2022, TUI***, Jet2, On The Beach****, Love Holidays and easyJet Holidays***** now account for 62% of the package market, an increase from 52% in 2017 and 53% in 2019.

The top ten now represent a staggering 75% of the market up from 62% in 2017.

We believe this increased consolidation is primarily down to funding.

Larger ATOL holders have generally found it easier to raise new money from various sources – such as rights issues, issuing bonds, increasing loan and revolving credit facilities, selling non-core assets, sale and leasebacks, or accessing government support schemes.

Conversely, small and mid-sized operators have found it harder to raise funds. Many have survived the last couple of years through day-to-day firefighting and a strong focus on cost control. They now find themselves with weakened balance sheets, making it more expensive for them to satisfy regulators’ requirements. As a result, they are generally more cautious about increasing licence limits given the uncertain economic outlook.

If you would like more insights to help guide your business strategy, please get in touch.

**Number of ATOL holders with public sales greater than zero, therefore excludes Transport Company ATOL holders, many of whom allowed their Transport ATOLs to lapse.

***Includes Marella Cruises ATOL ****Includes Classic Collection ATOL *****Includes easyJet Airline ATOL

Join our newsletter

If you enjoyed this post, why not sign up to our newsletter? Get our latest blog posts, industry updates and exclusive content.

Sign up