ABTA announced a string of rule changes ahead of the September 2023 renewal aimed at simplifying and modernising its approach to assessing and monitoring members.

In this post, we explore the four key changes.

1 – New financial criteria

ABTA is reintroducing financial tests for both Principal and Retail members in an effort to establish a minimum financial strength across its membership.

You’ll have three years to transition to the new financial criteria if you’re an existing ABTA member. But anyone applying as a new member will need to meet the tests immediately.

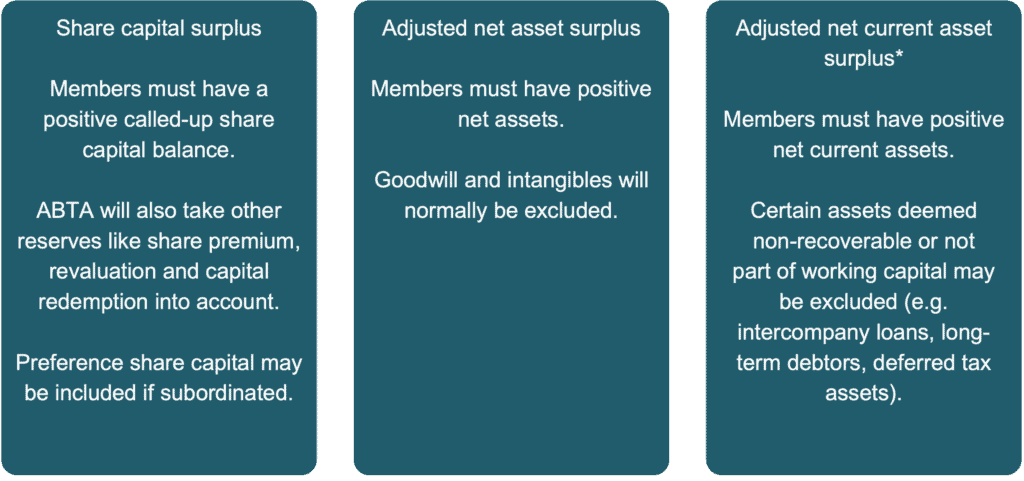

The three new financial tests that all ABTA members should meet.

All ABTA member’s latest financial accounts will need to show:

An extra financial test for the ABTA Bond+ scheme

In addition, if you’re an ABTA Principal member and you want to take advantage of a lower Principal Bond under the Bond+ scheme (covered below), you’ll need to meet an extra financial test to be eligible:

2 – New Bond+ scheme for ABTA Principals

ABTA changed its bond calculation for Principal members during the pandemic, generally setting bonds at a level to cover the forecast peak balance of customer money expected to be held.

But as booking levels recovered, bond levels grew exponentially, and many members couldn’t find sufficient bond capacity to meet this requirement. In response, ABTA has introduced the Bond+ scheme.

At the time of renewal, members eligible for Bond+ will have the option to continue providing a bond covering the forecast peak customer money balance. Alternatively, you can elect to provide a lower bond in return for an increased payment into ABTA’s captive insurance fund.

To be eligible for Bond+, your accounts must meet the additional financial test: Net Recoverable Assets of more than 4% of your principal turnover.

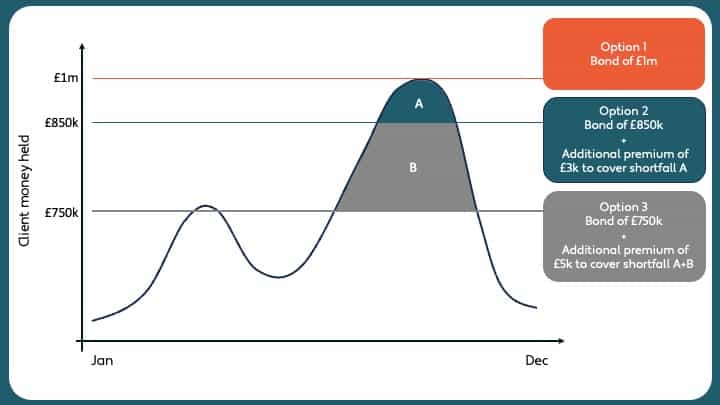

How does it work? Here’s an example.

At your annual renewal, ABTA will continue requesting a forecast of the balance of customer money you expect to hold at each month end.

The default bond option will be your customer money peak. Let’s say that’s £1m.

If you meet ABTA’s enhanced financial criteria, you will be offered the option to provide a lower bond of, for example, £850k.

ABTA’s captive insurance scheme will effectively be taking on the risk of the potential shortfall (in this case, £150k). So, there will be an additional insurance premium (“Principal Premium+”) to pay into ABTA’s captive insurance for the difference. The Principal Premium+ rate varies but is typically around 2% per year, making the cost of insuring the shortfall £3,000.

You may be offered a final option, of say £750k. In this case, the potential shortfall will be £250k, and the additional Principal Premium+ (assuming an annual rate of 2%) will be £5,000.

Note that in accordance with the rules set out in the Package Travel and Linked Travel Regulations 2018, the lowest Principal bond ABTA can accept is 10% of your principal turnover.

The attractiveness of the ABTA’s Bond+ scheme will depend on the premium ABTA is charging relative to your bond provider. But for some members, it might reduce costs and make life easier.

3 – New Retail Premium+ scheme for travel agents

ABTA is phasing out the Travel Agent Bond Replacement scheme (TABRS) for smaller agents and replacing it with this new Retail Premium+ scheme. If you’re a travel agent with ABTA applicable risk turnover under £500,000 and meet the new financial criteria, you could be eligible for this scheme.

This means you no longer have to provide a retail bond. Instead, you can choose to pay a premium to ABTA’s captive insurance.

Your Retail Premium+ will be calculated at 0.5% of your Applicable Risk Turnover, with a minimum of £1,500+IPT.

4 – Relaxed quarterly reporting requirements for small ABTA members

Finally, there’s some good news for smaller ABTA members on the administration front. If you provide a Principal bond to ABTA of less than £50,000 or you’re a retail member using Retail Premium+, you will no longer need to submit quarterly turnover reports.

This new set of rules that ABTA has introduced brings significant changes for members. If you would like help understanding how you are impacted, please get in touch with our friendly regulatory team.

If you liked this article, we think you’ll love these:

Join our newsletter

If you enjoyed this post, why not sign up to our newsletter? Get our latest blog posts, industry updates and exclusive content.

Sign up