For many years, Google’s relationship with the travel industry has been uneasy. It acts as both a supplier and a competitor, and its forays into metasearch including the launch of its recent hotel booking tool have certainly caused concern.

Right now though, the UK travel industry is dealing with a different sort of Google headache, this time related to the increasing cost of Google Ads.

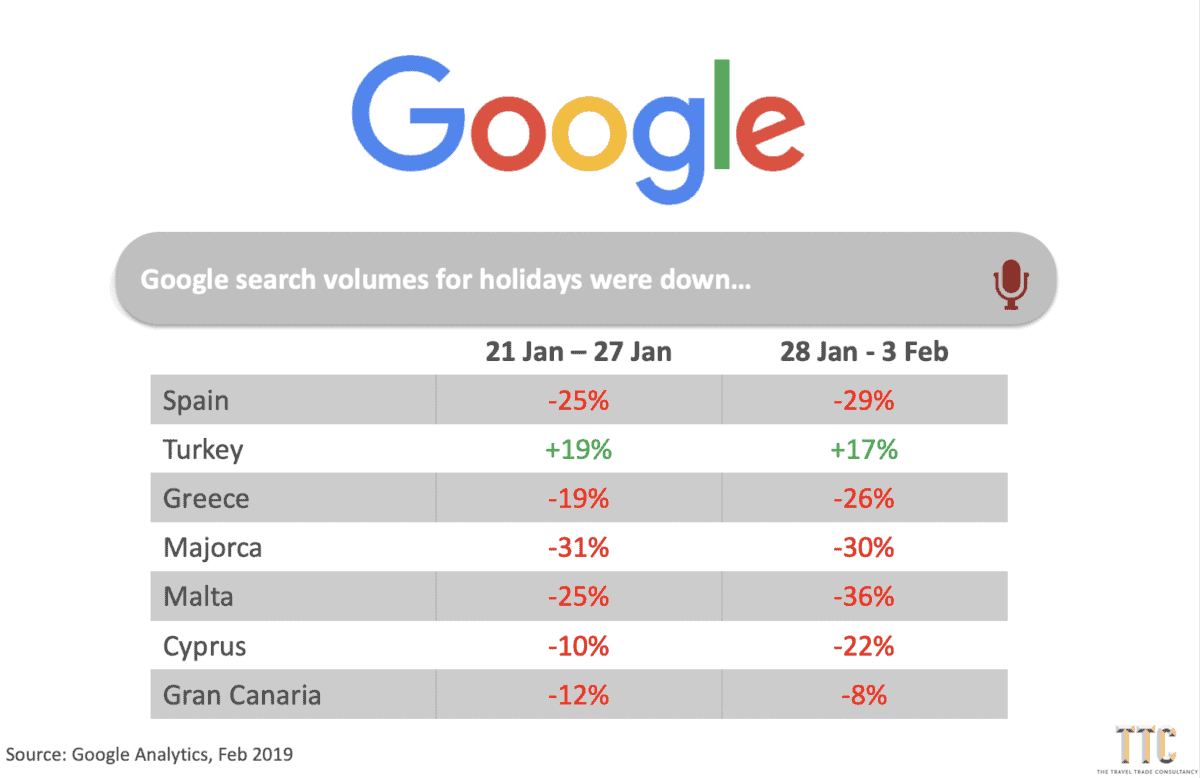

Google Ad Nauseous

So what exactly is the problem? Well, it’s largely to do with the fact that Google’s holiday search volumes in the UK are suffering in the current climate of low consumer confidence.

Take a look at the following summary of travel search terms from 2 specific weeks during the 2019 peak booking period, compared with the same weeks in 2018.

You’ll notice that apart from the one bright spot of Turkey, the other destinations in our research were all substantially down on search volumes. There are many possible explanations for such big drops. The latest booking data from GfK suggests a nervous consumer is certainly a big factor.

Whatever the reasons for the drop in search activity, many travel companies remain focussed on delivering a set number of enquiries into the top of their funnels, knowing they can rely on a certain percentage of them to convert into bookings. A scarcity of searchers drives up the cost per click and can dramatically increase the Customer Acquisition Cost.

A strictly non-scientific straw poll amongst our clients revealed their spend on Google Ads for Q1 2019 has risen anywhere between 6% – 20% compared to their spend on the same keywords in the equivalent period of 2018.

In any sector, that would be tough to take, but when you consider that some Online Travel Agents spend more than 50% of their net revenue on digital marketing, it’s clear that such cost increases are unsustainable.

Spreading the load

No doubt Google will continue to be the dominant digital market channel for the foreseeable future, but just like petrol prices during an oil price spike, when Google Ad costs go up, they don’t usually come back down again.

The step-change we’ve seen in early 2019 seems to be having a profound impact on business strategies in the sector.

More and more travel companies are looking to innovate away from Google and we are seeing our clients much more willing to diversify their marketing budget and experiment with alternative approaches.

Whether it be social media, voucher sites, flash sales, or metasearch. Each can seemingly deliver customers at a more attractive price point than Google right now.

A Non-Classic approach

Of all the innovations, the most eye-catching has been On The Beach’s (OTB) switch to offline sales following their purchase of Classic Collection in late 2018.

As a luxury tour operator with a large distribution network of high-street travel agents, Classic Collection is pretty much the antithesis of the Online Travel Agent.

However, OTB has been acting more and more like a traditional tour operator in recent years. They switched their legal status from agent to package organiser; they moved away from bed-banks and began contracting directly with hotels.

Now as a result of the acquisition of Classic Collection, they can distribute package holidays through offline, bricks and mortar travel agencies using the Classic Packages portal.

Selling package holidays on the high street is hardly a new idea, but shifting from online to offline flies in the face of conventional wisdom and could provide OTB with a natural hedge against the spiralling cost of digital marketing. That acquisition is looking smarter every day.